Introduction to Cost-Volume-Profit Analysis

Cost-Volume-Profit (CVP) analysis is an essential tool used in managerial accounting, serving to assess the interplay between a company’s costs, its sales volume, and its overall profitability. This analytical method provides significant insights that are crucial for decision-making processes in a variety of business environments. By understanding this relationship, managers can make informed choices about pricing, budgeting, and financial forecasting, ultimately supporting organizational goals.

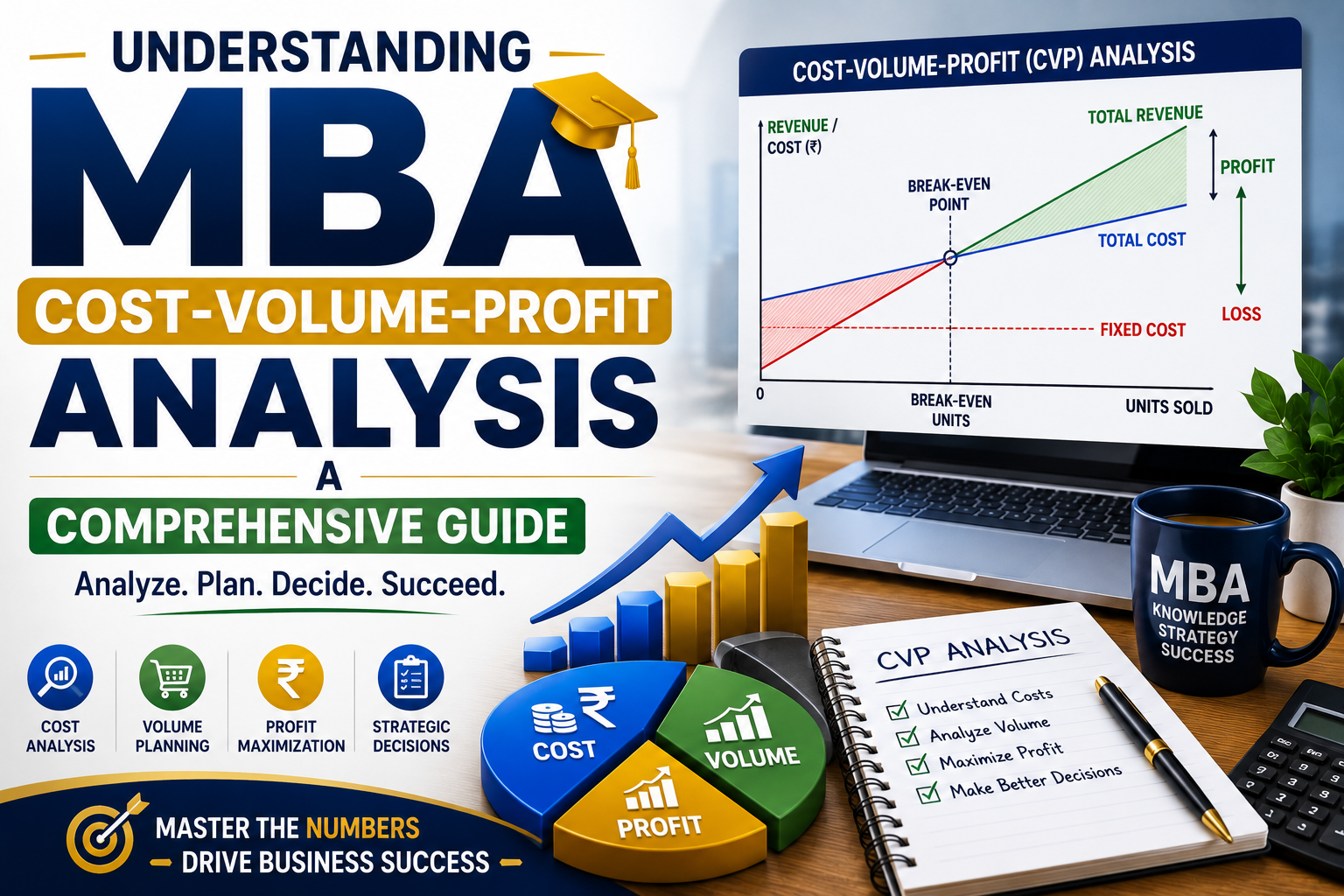

The foundation of CVP analysis lies in its ability to clarify how changes in cost structures and sales volumes affect a company’s bottom line. This relationship is commonly visualized through a CVP graph, which illustrates the break-even point—the threshold at which total revenues equal total costs. Below this point, a business incurs losses, whereas above it, profits are generated. Therefore, determining the break-even point is fundamental to business decision-making, allowing managers to establish sales targets that ensure profitability.

Moreover, CVP analysis incorporates fixed and variable costs, which are critical in this evaluation. Fixed costs do not change with sales volume, such as rent or salaries, while variable costs fluctuate directly with production levels, like materials and labor. By dissecting these costs, managers are better equipped to analyze how shifts in sales volume impact profitability, enabling the formulation of strategic plans tailored to specific market conditions.

Ultimately, the significance of CVP analysis extends beyond the confines of accounting. It fosters a deeper understanding of operational efficiency and decision-making strategies. As firms navigate complex financial landscapes, mastering the principles of cost, volume, and profit will empower them to adapt and thrive in competitive markets. In the subsequent sections, readers can expect to delve deeper into the intricacies of CVP analysis, further illuminating its role in effective business management.

Key Components of Cost-Volume-Profit Analysis

Cost-Volume-Profit (CVP) analysis is an essential financial tool that helps businesses assess their operational efficiency and profitability under varying conditions. The primary components of CVP analysis are fixed costs, variable costs, sales price per unit, contribution margin, and the breakeven point. Understanding these elements is vital for effective financial decision-making.

Firstly, fixed costs are expenses that do not change regardless of the level of production or sales. These may include rent, salaries, and insurance, which remain constant over a specific period. On the other hand, variable costs fluctuate directly with production or sales volume. Examples include materials, labor directly involved in manufacturing, and sales commissions. The relationship between these two cost categories is crucial, as it influences the overall profitability of a business.

The sales price per unit is another critical component, representing the amount charged to customers for each unit sold. This price must align with the market demand and competitive landscape to ensure sales volume meets or exceeds the costs incurred. The contribution margin, derived from the sales price per unit minus variable costs, represents the amount available to cover fixed costs and contribute to profit. A higher contribution margin indicates a more profitable product.

Finally, the breakeven point is the level of sales at which total revenues equal total costs, resulting in neither profit nor loss. Understanding the breakeven point is critical for businesses, as it assists in setting sales targets and pricing strategies. The interplay of fixed costs, variable costs, sales price per unit, contribution margin, and breakeven point creates a comprehensive framework for decision-makers to evaluate profitability and make informed strategic choices in their operations.

The Concept of Breakeven Analysis

Breakeven analysis is a critical financial tool utilized by businesses to determine the point at which total revenues equal total costs, resulting in neither profit nor loss. This point is known as the breakeven point (BEP), and it serves as a pivotal indicator for financial decision-making and strategic planning. Understanding the breakeven point allows businesses to set sales targets, assess the viability of new products or services, and make informed decisions regarding pricing and cost management.

To calculate the breakeven point, several approaches can be utilized. One common method involves the use of a formula that considers fixed and variable costs. The formula is expressed as: BEP = Fixed Costs / (Selling Price per Unit – Variable Cost per Unit). This straightforward calculation effectively provides the minimum quantity of sales needed to cover all costs, ensuring that businesses can assess how much product they must sell before they start making a profit.

Alternatively, breakeven analysis can also be depicted graphically. A breakeven chart plots total revenue and total cost on the same graph, highlighting the point where the two lines intersect. This visual representation simplifies the process of understanding how different pricing strategies or cost structures can impact overall profitability. It emphasizes the importance of understanding cost behavior, thereby enhancing strategic financial planning.

The implications of breakeven analysis extend into areas such as financial planning and risk management. By identifying the breakeven point, companies can evaluate the risks associated with changes in costs or sales volume. This analysis aids firms in making informed choices to mitigate potential risks while ensuring long-term sustainability. Ultimately, a thorough grasp of breakeven analysis allows businesses to navigate complex financial landscapes with greater confidence, making it an essential component of comprehensive financial strategies.

Understanding Contribution Margin

The concept of contribution margin is pivotal in both managerial accounting and financial analysis, especially in relation to cost-volume-profit (CVP) analysis. Contribution margin is calculated by subtracting variable costs from total revenue. This metric reflects the portion of sales revenue that exceeds total variable costs, generating funds to cover fixed costs and consequently contributing to profit. The formula is expressed as: Contribution Margin = Sales Revenue – Variable Costs.

<punderstanding a=”” align=”” allocated=”” alternatives.<pit (cogs),=”” a=”” accounts=”” affect=”” analysis.<pin accurately=”” an=”” analysis=”” and=”” assess=”” between=”” broader=”” businesses=”” by=”” context=”” contribution=”” cost-volume-profit=”” costs,=”” decisions.=”” empowers=”” encapsulating=”” facilitates=”” financial=”” frameworks.

Applications of Cost-Volume-Profit Analysis

Cost-Volume-Profit (CVP) analysis is a powerful tool utilized by businesses to make informed decisions regarding pricing strategies, product line selection, budgeting, and forecasting. One of the primary applications of CVP analysis lies in its ability to aid businesses in establishing an optimal pricing strategy. By understanding the relationship between cost, sales volume, and profit, companies can set prices that ensure profitability, taking into account fixed and variable costs.

For instance, a manufacturing company may employ CVP analysis to determine the break-even point at which its total revenues equal total costs. Through this analysis, the company can ascertain how many units must be sold to achieve profits while considering both fixed costs, such as rent and salaries, and variable costs, such as materials and labor. This critical insight allows businesses to assess the feasibility of different pricing strategies and refine their approach to maximize profits.

Moreover, CVP analysis plays a vital role in product line selection. Companies often evaluate different products to determine which offerings yield higher profitability. By analyzing the cost and volume associated with each product line, businesses can prioritize those that contribute more significantly to their bottom line, ultimately driving strategic decisions about production and marketing efforts.

Budgeting is another area where CVP analysis proves invaluable. This tool assists in forecasting future financial performance by enabling companies to explore different scenarios and assess the implications of changes in costs and sales volumes. For example, a retail company could predict how a shift in consumer demand might influence its sales volume and revenues, allowing it to adjust its budget accordingly.

In conclusion, Cost-Volume-Profit analysis is integral in guiding various business decisions, from pricing strategies and product selections to budgeting and forecasting. Numerous companies across different industries utilize this analysis to optimize profitability and enhance decision-making processes.

Limitations of Cost-Volume-Profit Analysis

Cost-Volume-Profit (CVP) analysis is a widely used financial tool that assists businesses in understanding the interrelationship between costs, sales volume, and profitability. However, this analytical framework does have inherent limitations that must be acknowledged. One of the primary assumptions of CVP analysis is linearity, which implies that costs and revenues change in a straight line relative to volume. In reality, many businesses experience variable costs that do not follow a linear pattern, particularly as production levels increase or decrease.

Another critical assumption is that the selling price remains constant, regardless of changes in market conditions, demand, or competitive pressures. Price fluctuations can greatly impact a company’s profitability, potentially leading to misleading conclusions if CVP analysis is employed in scenarios where the assumption of constant selling price does not hold. This inflexibility can limit the practicality of CVP in dynamic markets where prices are subject to significant changes.

Moreover, CVP analysis is often considered less applicable to diverse business models, particularly in industries that rely on multiple products or services with varying cost structures and profit margins. In such cases, a simplistic application of CVP may not provide an accurate picture of a company’s financial health, as it fails to account for the complexities of multi-product cost behavior.

Additionally, over-reliance on CVP analysis can pose pitfalls for decision-making. It may lead to a narrow focus on short-term profitability at the expense of long-term strategic planning, thus neglecting other essential financial metrics. This limitation underlines the importance of using CVP analysis in conjunction with other financial assessment tools to deliver a balanced perspective on business performance and long-term viability.

Comparative Analysis with Other Financial Tools

Cost-Volume-Profit (CVP) analysis is a fundamental financial tool that assists businesses in understanding the relationship between costs, sales volume, and profit. By analyzing these elements, CVP can provide critical insights that influence decision-making. When comparing CVP analysis with other financial management tools such as budget variance analysis and break-even/target costing, distinct differences in their applications and benefits emerge.

Budget variance analysis focuses primarily on discrepancies between planned budgets and actual spending. It identifies areas where a company may be overspending or underperforming against its financial projections. While this tool helps organizations stay on track with their financial goals, budget variance analysis is retrospective, analyzing past performance rather than predicting future scenarios. In contrast, CVP analysis is proactive; it allows businesses to forecast the effects of changes in costs and volume on their overall profit. This forward-looking capability makes CVP a vital tool in strategic planning.

Break-even analysis, often integrated within CVP analysis, specifically calculates the sales volume needed for a business to cover its costs, leaving no profit or loss. Target costing, on the other hand, determines the desired cost of a product based on its market price and required profit margin, guiding product development toward those financial targets. While both break-even analysis and target costing offer valuable insights into cost management, CVP analysis encompasses a broader scope, linking costs, sales volume, and profit into a cohesive framework that can aid in pricing, product mix, and sales strategies.

Ultimately, understanding when to employ CVP analysis versus other financial tools can empower managers to make more informed decisions. Each method has its strengths, but CVP’s unique capability to project financial outcomes based on variable costs and sales levels makes it particularly useful in uncertain market conditions.

Case Studies: Real-Life Applications of CVP Analysis

Cost-Volume-Profit (CVP) analysis serves as an invaluable tool for businesses in strategizing their operations and financial planning. To illustrate its practical use, we will examine a few notable case studies that highlight how various companies have successfully implemented CVP analysis to drive their decision-making processes.

One prominent example is the international fast-food chain, McDonald’s. Faced with rising operational costs and fluctuating customer demand, McDonald’s utilized CVP analysis to reassess its pricing strategy and product offerings. By determining their break-even point, they recognized the necessity to adjust menu prices while considering overall customer turnout. This analysis led to the introduction of value meals, which not only increased sales volume but also ensured profitability even with competitive pricing. The successful integration of CVP in their strategy confirmed McDonald’s resilience in a rapidly changing market environment.

Another illustrative case is that of Dell Technologies, which leveraged CVP analysis in its direct-to-consumer sales model. By evaluating the relationships between fixed costs, variable costs, and expected sales volume, Dell was able to identify an optimal production strategy. This allowed them to innovate and offer customized technology solutions without incurring excessive costs. The outcome was a lean operation that successfully catered to the increasingly diverse consumer preferences while maintaining healthy profit margins, showcasing the effective use of CVP analysis in the tech industry.

Lastly, the retail brand, Target, utilized CVP analysis to optimize its inventory management model. During a period of economic downturn, Target faced pressure to generate higher profits while managing overhead costs. By applying CVP analysis, the company could strategically evaluate the impact of sales forecasts on profit margins. Consequently, this led to targeted markdown strategies that not only alleviated excess inventory but also increased customer traffic, demonstrating how CVP can guide critical business decisions in a retail context.

Conclusion: The Importance of Cost-Volume-Profit Analysis in Business Strategy

In summary, Cost-Volume-Profit (CVP) analysis serves as an essential tool for organizations aiming to navigate the complexities of financial decision-making. Throughout this guide, we have highlighted how CVP analysis assists businesses in understanding the interplay between costs, sales volume, and profitability. By effectively utilizing CVP analysis, managers can make informed decisions regarding pricing strategies, product emphasis, and resource allocation, which directly influence the financial health of the organization.

Moreover, the insights gained from CVP analysis are invaluable for budgeting and forecasting. As organizations face continuous changes in the market dynamics, the ability to predict how changes in costs and sales volumes will affect profits is critical. By leveraging this analysis, businesses can devise strategic plans that are not only reactive but also proactive in facing challenges and seizing opportunities.

It is vital for organizations to integrate CVP analysis into their strategic planning processes. Implementing this approach can lead to improved clarity in financial projections and a more robust understanding of risk. Businesses can assess various scenarios—such as fluctuating sales volumes or alterations in cost structures—thereby enhancing their agility and resilience in today’s competitive landscape.

As we conclude, we encourage readers to reflect on how they might incorporate CVP analysis into their own business frameworks. By doing so, organizations can beyond traditional metrics and adopt a holistic view of financial performance, which is crucial for maintaining a competitive edge. As the business environment continues to evolve, embracing tools like CVP analysis will be key to driving sustainable growth and informed decision-making.